After my departure from 4 Pillars Consulting Group, in February of 2010, I have often wondered how this organization continues to avoid Provincial and Federal Legislation that was clearly written with the 4 Pillars debt consulting services model in mind. From providing individual debt settlements on behalf of debtors with collection agencies and their creditors to negotiating with Trustees on behalf of a debtor in determining the terms of a Consumer Proposal, at no time did the organization feel that they ought to have any oversight in what they did. Myself, I had a number of debates with Robert Glen, the 4 Pillars manager in Windsor, Ontario with issues on our true value to a debtor when first, the authorizations that we would send had no determinant weight, as collection agencies and creditors could simply ignore them, without recourse. Second, we would tell the debtor that we were “representing” them and their interests in the Consumer Proposal, Bankruptcy or Debt Settlement process, yet we were not licensed to provide advice by any calculation within the confines of any regulatory statute, or the Law Society Act.

Moving ahead, I recall a time in December of 2014, while speaking with my wife and owner of New Beginnings Debt Consulting at the time, that there were new changes in the Collection Agency Act of Ontario that was going to have a significant impact on how we conduct business and interact with the public. I even reached out to Reginald Rocha, 4 Pillars Director and Partner, to discuss the changes in the Act, as we shared a common model in negotiations with the various players in the Debt Settlement Industry. You see, the Ontario government had recently enacted the new Collection Agency Act to its current name the Collection and Debt Settlement Services Act. As with any changes in legislation I consulted with our Lawyers and they agreed that these new changes affected how we would interact with the public, but more importantly that registration with the Ministry of Government and Consumer Services would be a requirement and would come into effect as of June 1st, 2015. I had asked if there was a way that I could become exempt and was informed that if I became a licensed trustee or a lawyer, I would be provided with exemption status and could continue to negotiate settlements with Trustees, collection agencies and creditors without the registration requirement.

After thoughtful consideration, I chose to become a Licensed Paralegal with the Law Society of Ontario and although it did not provide me with immediate exemption status, it did provide me with standing when dealing with a debtor’s Trustee, Creditors and Collection Agencies. As discussed before, I had great issue and concern that while with 4 Pillars, we were passing along these authorizations and telling debtors that this authorization gave us authority to speak to their creditors on their behalf while we were negotiating a client’s debt with a Trustee or negotiating an individual settlement. Now that I became licensed as a Paralegal I had standing and my authorizations carried weight. Section 22(2) of Regulation 74 of the Collection and Debt Settlement Services Act essentially says that at no time may a creditor, collection agency or agent in the collection of a debt contact a debtor upon being notified that the debtor has hired a legal practitioner in the negotiation of a debt. Now I could provide legal advice to my clients. At that time, in order to become compliant with the law, my practice registered with the Ministry and until just recently, in August of 2018, Paralegals have now gained exemption status and are now free from that burden.

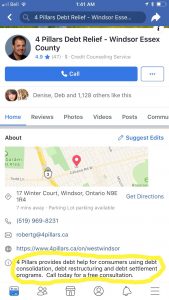

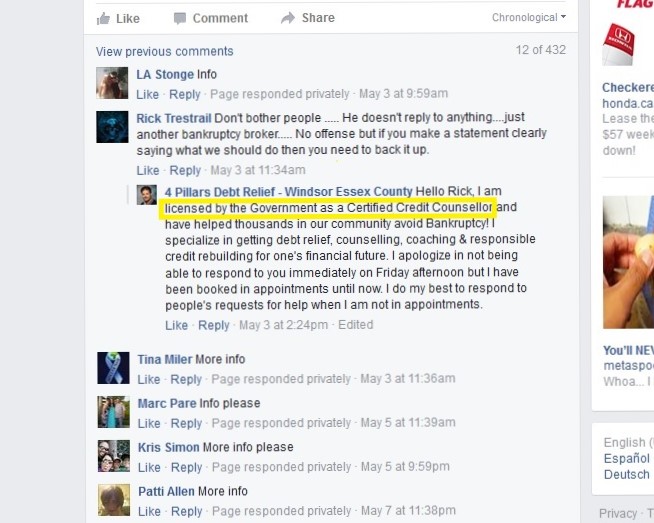

I did, however, find it troubling that 4 Pillars never registered with the Ministry. I don’t believe any of them are lawyers. I do recall a conversation with Robert Glen, the 4 Pillars manager in Windsor, Ontario about a year ago that he wanted to go back to school and get a Law Degree. Being a lifelong, family friend, I told him he would make a great lawye, although he indicated that his corporate offices in British Columbia told him that he would have to give up his franchise. I know many have become Credit Counselors in attempt to give them some sort of status or credibility in the industry. Recently, however, the Office of the Superintendent of Bankruptcy (OSB) has threatened to revoke many of their credit counseling registrations as the OSB had discovered that trustees were handing off debtors back to the 4 Pillars agent and paying 4 Pillars the $75 counseling fee for each session. The OSB then made changes to how Trustee’s conduct themselves and under the new Directive No. 1R4 (https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/br03864.html), a Trustee cannot send a debtor to a credit counselor who was referred to the Trustee originally do have unless the Trustee places the credit counselor under the Trustee’s license. I will note that although Credit Counselors are registered with the OSB, they do not provide oversight of Credit Counselors, are not licensed and thusly have no legal standing or authority under past or current law to address a debtor’s needs.

Recently, I came across an article by Mr. Mark Silverthorn. Mr. Silverthorn equates himself as having a great deal of knowledge in the Debt Industry, and although we have quarreled from time to time, I do have a great deal of respect for him and the expertise he carries in our industry. Mr. Silverthorn wrote an article, entitled; “Debt Relief Industry Commentator Mark Silverthorn Predicts Potential Fallout from Four Pillars’ Defamation Lawsuit Against Victoria Trustee Colleen Craig”. I will say that I had come across Ms. Collen Craig’s blog a few years ago regarding her position with how 4 Pillars conducts themselves in Victoria. From my own personal experience with working at 4 Pillars, her assessment is truly spot on!